EV battery innovation and thermal stability needs fuel adoption

ROCKVILLE, MD, UNITED STATES, April 16, 2026 /EINPresswire.com/ — According to the latest analysis by Fact MR, Germany is solidifying its position as a global nerve center for advanced battery materials, with the Lithium Bis(fluorosulfonyl)imide (LiFSI) Electrolyte Salt market poised for a transformative decade. As the European automotive powerhouse pivots toward next-generation Electric Vehicle (EV) architectures, LiFSI has emerged as the critical “enabler” for high-voltage and high-energy-density cells.

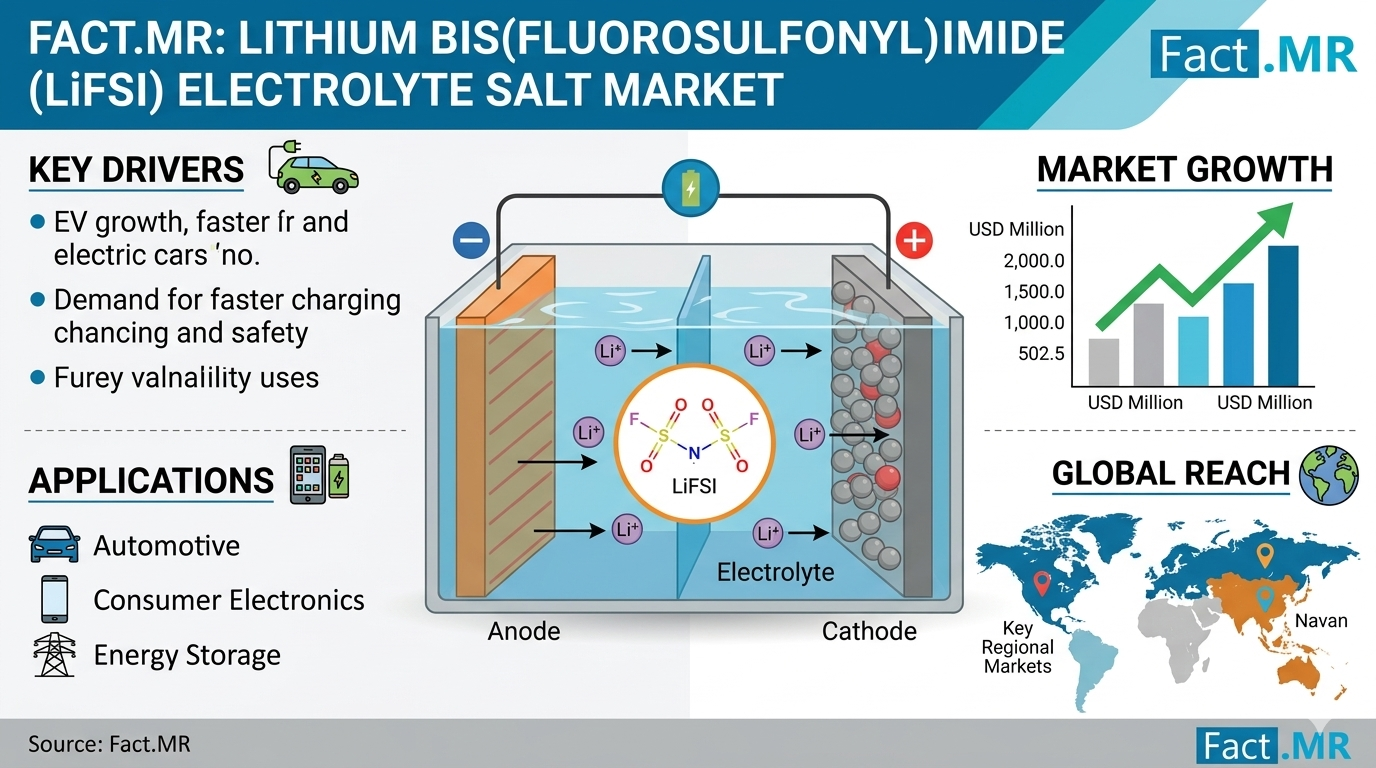

Valuation of the Lithium Bis(fluorosulfonyl)imide (LiFSI) electrolyte salt market is projected to grow from USD 1.3 billion in 2025 to USD 1.6 billion by 2026. Intensifying R&D and the expansion of domestic gigafactories are expected to propel the market to a staggering USD 5.4 billion by 2036. This represents a robust CAGR of 13.9% for Germany, outpacing many other mature markets and creating an incremental opportunity of USD 3.8 billion.

Get detailed market forecasts, competitive benchmarking, and pricing trends:

https://www.factmr.com/connectus/sample?flag=S&rep_id=14726

Quick Stats Section

Market Size (2026E): USD 1.6 Billion

Projected Value (2036F): USD 5.4 Billion

Germany CAGR (2026–2036):9%

Incremental Opportunity: USD 3.8 Billion

Leading Segment (Application): Lithium-ion Batteries (64% share)

Leading Purity Level: Above 99.9% Purity (55% share)

Key Regional Players: BASF SE, Merck KGaA, Arkema S.A., Solvay S.A., Nippon Shokubai Co. Ltd.

Executive Insight for Decision Makers

The market is undergoing a fundamental strategic shift. While Lithium Hexafluorophosphate ($LiPF_6$) has long been the industry standard, its thermal limitations at high voltages are becoming a bottleneck for the EV industry. OEMs and battery manufacturers must now prioritize the integration of LiFSI to meet consumer demands for faster charging and longer cycle life.

“Germany is functioning as the advanced battery materials regulatory laboratory for Europe,” states a Principal Consultant at Fact MR. “Investors and manufacturers who fail to adapt to these high-purity, fluorinated salt chemistries risk exclusion from the next generation of solid-state and high-nickel battery supply chains.”

Market Dynamics

Key Growth Drivers:

EV Battery Evolution: Demand for salts that facilitate stable Solid Electrolyte Interphase (SEI) layers in high-nickel cathodes.

EU Regulatory Frameworks: Support from the European Battery Alliance (EBA) for localized, high-performance material production.

Thermal Management: Superior performance of LiFSI in extreme temperature ranges compared to legacy salts.

Key Restraints:

Synthesis Complexity: Multi-step fluorination processes lead to higher per-unit pricing.

Corrosion Challenges: Requirement for specialized aluminum foil protection in current collectors to prevent LiFSI-induced corrosion.

Emerging Trends:

Dual-Salt Electrolytes: Combining $LiPF_6$ and LiFSI to balance cost and performance.

Solid-State Integration: LiFSI’s role as a primary conductive salt in hybrid and solid polymer electrolytes.

Segment Analysis

In 2026, Lithium-ion Batteries are projected to dominate with a 64% share, driven by the immediate needs of the passenger EV market. However, the Above 99.9% Purity segment is the most strategically significant, holding 55% of the market. This high-purity threshold is non-negotiable for German manufacturers, as even trace metallic impurities can lead to parasitic reactions that degrade expensive battery packs prematurely.

Supply Chain Analysis: The Fluorine Factor

The supply chain for LiFSI is a specialized ecosystem:

Raw Material Suppliers: Providers of high-purity lithium and specialized fluorinating agents.

Manufacturers/Producers: Specialty chemical giants like BASF SE and Arkema who handle the complex synthesis.

Distributors: Specialist chemical distributors ensuring “clean-room” logistics to prevent moisture contamination.

End-Users: Gigafactories (e.g., Northvolt, Tesla Giga Berlin) and tier-1 auto OEMs like Volkswagen and Mercedes-Benz.

“Who Supplies Whom”: In Germany, domestic leaders like Merck KGaA supply high-purity additives and salts to electrolyte formulators, who then deliver customized blends to cell manufacturers.

Pricing Trends

Premium Chemistry: LiFSI remains a premium-priced material compared to $LiPF_6$ due to the complexity of sulfur-fluorine bond synthesis.

Influence Factors: Pricing is sensitive to the cost of fluorine precursors and the stringent energy requirements of purification.

Margin Insights: Manufacturers maintaining a 9%+ purity standard command significantly higher margins, as battery grade consistency is the primary barrier to entry.

Regional Analysis: Germany’s Dominance

While the United Kingdom leads the growth curve at 14.2%, Germany follows closely at 13.9%. Germany’s growth is anchored by its unmatched industrial infrastructure and the “France 2030” and “European Battery Alliance” frameworks that incentivize localized chemical production. This allows German firms to avoid the supply chain volatility associated with importing materials from Asia.

Competitive Landscape

The market is moderately consolidated, led by firms with deep expertise in fluorochemicals.

Key Strategies: Players like Nippon Shokubai and Solvay are focusing on scaling production to drive down costs, while Merck KGaA and BASF are doubling down on “Performance Chemicals” to offer proprietary electrolyte blends.

Market Structure: A blend of global chemical conglomerates and specialized regional producers.

Strategic Takeaways

For Manufacturers: Invest in aluminum-passivation technology to mitigate the corrosive nature of LiFSI at high concentrations.

For Investors: Focus on companies with patented, low-waste synthesis pathways for fluorosulfonyl groups.

For Marketers: Position LiFSI not as a replacement for $LiPF_6$, but as a “performance booster” essential for high-voltage applications.

Future Outlook

By 2036, the “Dual-Salt” approach will likely become the global standard, with LiFSI playing a major role in the transition to Solid-State Batteries. As Germany moves toward a circular economy, the recyclability of fluorinated salts will become the next major technological frontier, offering long-term sustainability opportunities for the chemical industry.

Conclusion

The German LiFSI market is at a tipping point. As the automotive industry shifts from “early adoption” to “mass electrification,” the demand for the chemical precision offered by LiFSI will be the difference between a competitive EV fleet and an obsolete one.

Why This Market Matters

The battery is the heart of the energy transition, and the electrolyte salt is its lifeblood. LiFSI represents the pinnacle of current electrochemical stability, ensuring that the next generation of German-made EVs are not only faster and longer-lasting but also inherently safer.

Full Report: Unlock 360° insights for strategic decision making and investment planning-

https://www.factmr.com/checkout/14726

To View Related Report:

Lithium Extraction Chemicals Market https://www.factmr.com/report/lithium-extraction-chemicals-market

Lithium-ion Battery Binders Market https://www.factmr.com/report/lithium-ion-battery-binders-market

Lithium Mining Market https://www.factmr.com/report/lithium-mining-market

Lithium-ion Battery Recycling Market https://www.factmr.com/report/lithiumion-battery-recycling-market

S. N. Jha

Fact.MR

+1 628-251-1583

email us here

Legal Disclaimer:

EIN Presswire provides this news content “as is” without warranty of any kind. We do not accept any responsibility or liability

for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this

article. If you have any complaints or copyright issues related to this article, kindly contact the author above.

![]()

Media gallery